What Is A Bank Wire Transfer? The No-Nonsense Guide.

Look, you waa know what a bank wire transfer is? It’s simple. It’s moving money. Fast. Between banks. Electronically. Forget snail mail checks or waiting days for ACH. This is the heavy artillery of money movement. This is how big deals get done. This is how you pay for that sweet classic car you found online, or how a business closes a crucial acquisition. Honestly, it’s been around forever, way before your fancy fintech apps. It’s a trusted, albeit sometimes expensive, method.

:max_bytes(150000):strip_icc()/wiretransfer-FINAL-8fb2c62ec7e7410792ebb33a8c82ddb9.jpg)

The thing is, wire transfers are different. They’re not like your everyday debit card swipe or a peer-to-peer payment app. This is serious business. We’re talking about a direct instruction from one bank to another. No middlemen mucking about. Just pure, unadulterated cash flow. It’s secure, it’s fast, and it usually costs you. A lot.

Why Bother With Wires?

Speed. That’s the first thing. Need cash moved yesterday? A wire’s your guy. Need to buy a house? Closing day demands it. Need to send money internationally for that urgent business deal? Wires are king. They’re the quickest way to get large sums of money from Point A to Point B, across town or across the globe, without physically hauling cash around. It’s a modern solution to an age-old problem: getting paid, or paying up, without the wait.

:max_bytes(150000):strip_icc()/bank-wire-transfer-basics-315444_v3-188d0ebbe9754fcbb7a2bb37b2bdde37.jpg)

Consider this: I once had to wire $50,000 for a down payment on a property. My loan officer was breathing down my neck. The seller’s agent was twitchy. A bounced check? Nightmare. A delayed ACH? Unthinkable. The wire went through in hours. Peace of mind? Priceless. The fee? Aoying, but worth every pey.

How Does This Magic Happen?

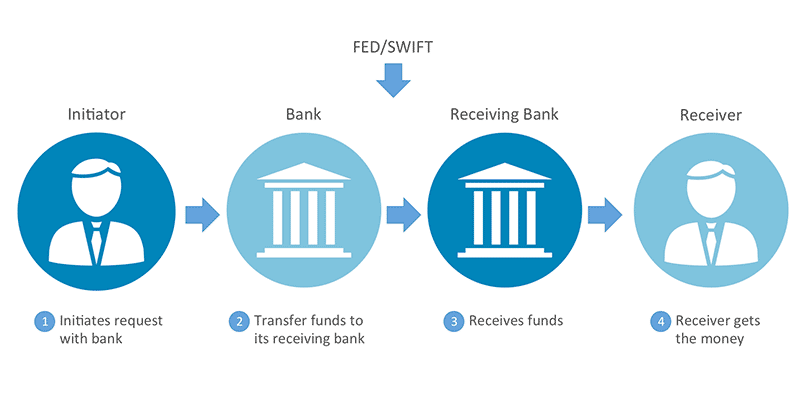

It all starts with you. You walk into your bank. Or, if you’re lucky and your bank’s got its act together, you do it online. You fill out a form. It’s not rocket science, but you gotta get the details EXACTLY right. Think of it like a missile lock. One wrong digit, and that money’s going on a joyride. You need:

- The recipient’s name. Duh.

- Their bank’s name and address. Don’t guess.

- Their account number. The golden ticket.

- Routing numbers. Crucial for domestic.

- SWIFT/BIC codes for international. The global GPS.

Your bank then uses the Fedwire (for domestic in the US) or SWIFT network (for international) to send the instruction. Your bank essentially tells their bank, “Hey, send $X to this person, it’s coming from us.” The money moves electronically. Fast. No bags of cash changing hands. It’s clean. It’s efficient. It’s done.

:max_bytes(150000):strip_icc()/how-to-do-a-bank-wire-315450-v4-5b4766e2c9e77c001a2e43f8.png)

Domestic vs. International: What’s the Beef?

Domestic wires? Those are within the same country. Usually cheaper, faster, and simpler. Think moving money from your savings account in New York to your buddy’s account in California. Easy peasy. You’ll use routing numbers.

International wires? That’s where it gets spicy. You’re crossing borders. Different currencies, different banking systems, more regulations. It takes longer. It costs more. And there are more chances for things to go sideways. You’ll need SWIFT codes (Society for Worldwide Interbank Financial Telecommunication) and possibly intermediary banks. Honestly, if you can avoid international wires, you might want to. But sometimes, there’s no other way.

I remember sending money to my cousin in Germany. The fee was higher than expected. Took two days, not one. And the exchange rate? Let’s just say my cousin got less than I thought. You gotta factor in all those hidden costs and time delays.

The Cost: Prepare Your Wallet

Here’s the kicker. Wires ain’t free. They’re a premium service. Domestic wires can run you anywhere from $20 to $50. International wires? Start at $40 and can easily go north of $100, depending on the banks and the amount. And that’s just the sending fee! The receiving bank might charge you too. Plus, currency conversion fees if you’re going international. It adds up. Fast.

To be fair, some banks try to sweeten the deal. Maybe they waive the fee if you have a certain account balance. Or maybe they offer better exchange rates for larger sums. But generally, expect to pay. It’s the price of speed and certainty.

So, When Do I Actually USE This Thing?

Look, not for your morning coffee. This is for the big leagues:

- Real Estate Transactions: Down payments, closing costs, buying property. The ultimate use case.

- Large Purchases: Cars, boats, expensive collectibles. Anything where you need to prove funds moved immediately.

- Urgent Business Payments: Supplier invoices, payroll in a pinch, urgent vendor payments.

- International Fund Transfers: When speed is critical and other methods are too slow.

- Sending Money to Family in Emergencies: When they need cash NOW.

If you’re just sending your buddy $50 for pizza? Use Venmo. Use Zelle. Use whatever your damn phone app is. Wires are for when the stakes are high and time is short.

The Risks: Don’t Be Stupid

Wires are generally safe. BUT. And it’s a big BUT. They are irreversible. Once that money is gone, it’s GONE. Scammers love wire transfers for this reason. They pressure you. They tell you it’s urgent. They give you fake invoices. You wire the money. Poof. Gone forever. Never send money via wire transfer to someone you don’t know or trust implicitly. Especially if they’re pressuring you or asking for gift cards on top of the wire.

Double, triple, quadruple check those account numbers and routing/SWIFT codes. A typo can send your money to the wrong account. Good luck getting it back. It’s a bureaucratic nightmare. Maybe possible, maybe not. Don’t bet on it.

A Quick Peek at the Networks

Behind the scenes, a few key networks make this all happen:

| Network | Purpose | Speed | Cost (Typical) |

|---|---|---|---|

| Fedwire (US) | Domestic US Transfers | Real-time / Same Day | $25 – $50 (Sending) |

| CHIPS (US) | Large Value Domestic/Intl. | Settlement (Usually Same Day) | Varies (Often for Banks) |

| SWIFT (Global) | International Transfers | 1-5 Business Days | $40 – $100+ (Sending + Receiving + Intermediary) |

So you see, different networks, different rules, different costs. Fedwire is the workhorse for domestic US stuff. SWIFT is the global coector. CHIPS is more for interbank settlements, less for the average Joe, but it’s part of the plumbing.

What If My Bank Is Lame?

Not all banks offer easy online wire transfers. Some make you go in person. Some have strict limits. Some just suck. If your bank is being a pain, maybe it’s time to look elsewhere. Plenty of financial institutions, especially larger ones and credit unions, offer streamlined wire services. Do your homework. Compare fees. See who makes it easy.

I once had a small community bank that charged $75 for an outgoing domestic wire. Seventy-five bucks! I moved my business the next day. There are better options out there. Don’t settle for being ripped off.

Can I Get My Money Back?

This is the million-dollar question. Generally, no. Once a wire transfer is completed, it’s final. It’s like sending a registered letter. You can’t recall it once it’s delivered. If you were scammed, or sent money to the wrong account by mistake, your bank might try to help trace it or initiate a recall. But it’s not guaranteed. It’s a long shot. It can take weeks, months, or never happen at all. This is why accuracy and trust are paramount. The thing is, you’re instructing your bank to release funds irrevocably. Choose wisely. Double-check everything.

Alternatives to Wires?

Sure, if speed isn’t the absolute top priority:

- ACH (Automated Clearing House): Slower (1-3 days), much cheaper (often free), good for regular payments. Think direct deposit or bill pay.

- Certified Checks/Cashier’s Checks: Funds are guaranteed by the bank, but you have to physically deliver it. Slower than a wire.

- Money Orders: Low value, cheap, but slow and not for large amounts.

- P2P Apps (Zelle, Venmo, Cash App): Great for small, personal transfers between known individuals. Usually instant, but limits apply and not ideal for large, official transactions. Zelle is often integrated with banks and can be quite fast and free.

- Cryptocurrency: Fast, international, potentially cheaper BUT volatile, complex, and carries its own risks. Not for everyone.

For your typical house closing? Wires are usually the only game in town. For everything else, weigh the cost, speed, and risk.

The Bottom Line on Wires

What is a bank wire transfer? It’s a powerful, fast, electronic method of moving money between banks. It’s essential for large, time-sensitive transactions like real estate. It costs money. It requires precision. And it’s generally irreversible. Use it when you need speed and certainty for significant sums. Don’t use it for your lunch money. Understand the risks, verify every detail, and know your bank’s fees. That’s wire transfers. No fluff.

Frequently Asked Questions

How long does a bank wire transfer take?

Domestic wires typically arrive the same business day, often within hours. International wires can take 1-5 business days, sometimes longer, depending on the countries and banks involved.

Are bank wire transfers safe?

They are electronically secure, but the risk comes from human error or scams. Always double-check recipient details. Never wire money to someone you don’t know or trust implicitly. Wires are irreversible, making them a favorite for scammers.

What information do I need to send a wire transfer?

You’ll need the recipient’s full name, bank name and address, account number, and their bank’s routing number for domestic transfers. For international transfers, you’ll also need the SWIFT/BIC code and possibly an IBAN.

How much does a bank wire transfer cost?

Domestic wires can range from $20 to $50. International wires typically cost $40 to $100+, not including potential fees from intermediary or receiving banks and currency conversion charges.

Can I cancel a bank wire transfer?

Generally, no. Once the funds have been sent and received, wire transfers are considered final and irreversible. While banks may attempt a recall if requested immediately, success is not guaranteed.