The Tax-Free Gift Limit 2026: Don’t Get Screwed.

Look, nobody likes thinking about taxes. Especially not when you’re trying to be generous, right? You waa give your kid some cash for a down payment, help out a pal, whatever. Easy peasy. Except it ain’t. Not always. Especially when we’re talking about the Tax Free Gift Limit 2026. This whole thing? It’s a minefield. A damn minefield.

The IRS, bless their bureaucratic hearts, loves to tinker. They adjust these limits every damn year. Inflation, they call it. The real reason? Who knows. But the point is, what was okay last year might land you in hot water next year. And 2026? It’s goa be different. Mark my words.

I remember my Uncle Tony. He gave his grandkids a cool fifty grand, split between ’em. Thought he was being a good dude. Then BAM! Tax bill. He didn’t know from squat about the gift tax. Cost him more than the damn gift itself. Honest to God. Don’t be Uncle Tony.

Forget What You Think You Know. Now.

This whole ‘tax-free’ thing is a bit of a misnomer. It’s more like a ‘tax-deferred’ or ‘tax-limited’ situation. Unless you’re giving away pocket change, you gotta pay attention. The Tax Free Gift Limit 2026 isn’t some static number etched in stone. It moves. It breathes. It bites.

The thing is, most people just look at the aual exclusion. That’s the amount you can give to ANYONE, in any year, without using up any of your lifetime exemption. Sounds simple, right? Wrong. It’s the lifetime exemption that’s the real kicker. And that’s where things get hairy.

Remember 2017? The Tax Cuts and Jobs Act dropped this massive exemption. People thought they were golden. Gifted like there was no tomorrow. Well, guess what? That exemption was a temporary fix. It’s set to revert back. Or, at least, get adjusted. And 2026 is a big year for that adjustment.

The Big Kahuna: Lifetime Exemption

This is the big one. The amount you can give away over your entire life, both as gifts and through your estate, before the IRS starts taking a serious cut. For 2024, it was a whopping $13.61 million per person. Think about that. Thirteen. Million. Dollars. Most people ain’t gifting anywhere near that.

But here’s the gut punch: That $13.61 million number? It’s based on the 2017 Act’s generosity. That deal was set to expire after 2025. So, if Congress does NOTHING, and this is a huge ‘if’, the lifetime exemption is scheduled to drop. Significantly. We’re talking back down to around $5-6 million, maybe less, adjusted for inflation from 2011. That’s a massive haircut.

For 2026, the IRS will aounce the actual inflation-adjusted figures. But the writing is on the wall. Expect a BIG drop from the current highs. This means if you’ve been plaing large gifts assuming the $13 million+ exemption will stick around, you’re in for a rude awakening. The Tax Free Gift Limit 2026 is going to feel a lot tighter for big givers.

The Aual Exclusion: Still Matters, Kinda.

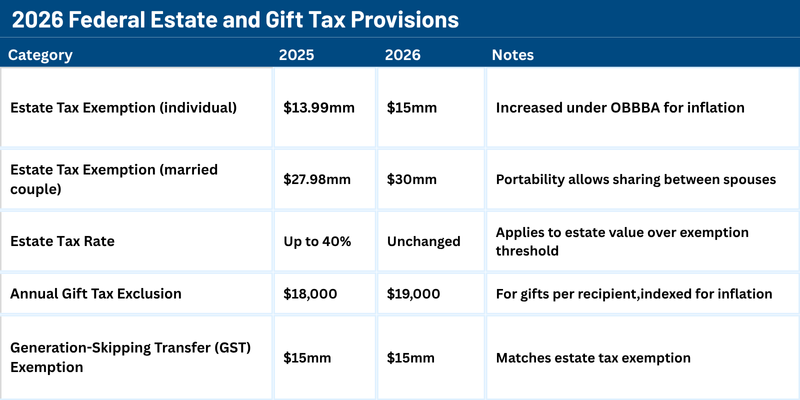

For 2024, the aual gift tax exclusion is $18,000 per recipient. That means you can give $18,000 to your son, $18,000 to your daughter, $18,000 to your cousin Mildred, and so on. All tax-free, no questions asked. And critically, it doesn’t touch your lifetime exemption.

For 2026, expect this number to creep up a bit due to inflation. Maybe $19,000? $20,000? It’s a decent buffer for smaller gifts. The problem isn’t the aual exclusion for MOST people. It’s when you start exceeding it, or when you’re dealing with massive estates where the lifetime limit becomes relevant.

My neighbor, bless her heart, she buys a new car for her grandson every year for his birthday. Drives me nuts. It’s like, $40k a pop. She just does it in chunks of $18k, thinking she’s beating the system. She’s not. The IRS sees the whole picture. That’s the kind of amateur hour that gets people busted.

Who Gets Hit? The Big Fish. And the Uninformed.

Let’s be clear. If your net worth is, say, under a million bucks, you’re probably not sweating the Tax Free Gift Limit 2026 lifetime exemption. You’d have to give away almost everything you own to even get close to the old numbers. The aual exclusion is your friend.

But for the ultra-wealthy? Or those sitting on appreciating assets? Or people who plan to pass down significant fortunes? This is HUGE. A drop in the lifetime exemption from $13.6 million to, say, $6 million is an extra $7.6 million that could be taxed at a hefty 40% rate. That’s serious cash gone up in smoke.

And the uninformed? Oh yeah. They get hit too. People who don’t do their homework. People who think ‘gift’ means ‘free money with no strings attached.’ Those are the ones who end up with surprise tax bills. It’s not pretty. I saw a guy once, thought he was clever gifting stock options. Ended up owing more in gift tax than the options were even worth at the time. Dumb.

The Plaing Nightmare: What The Hell Do I Do?

This is where the strategy comes in. And yeah, it requires actual thought. Not just throwing money around.

1. Know Your Numbers. Seriously. What’s your estate worth? What have you already gifted? What do you plan to gift? You need a clear picture. Don’t guess. Use spreadsheets. Use advisors. Use a damn crystal ball if you have to, but get the numbers straight.

2. Front-Load Your Gifting (Maybe). If you’re worried about the lifetime exemption dropping, and you have the assets, consider making larger gifts now or in the very near future. Use up some of that current, high exemption before it potentially shrinks. But this ain’t for everyone. Gotta have the liquidity. Gotta be sure you won’t need that cash yourself.

3. Utilize Trusts. Irrevocable trusts are your friend here. They can hold assets and be structured so that gifts to the trust don’t count against your direct lifetime exemption in the same way. It’s complex, sure, but it’s how the big boys play the game. And frankly, if you’re dealing with significant wealth, you should be thinking like the big boys.

4. Understand Spousal Rules. If you’re married, you and your spouse can combine your lifetime exemptions. You can also ‘gift split,’ meaning you can treat gifts made by one spouse as if they were made by both. This effectively doubles your combined aual and lifetime exclusions. More bang for your buck, tax-wise. But you gotta file the right forms. Form 709. Don’t forget it.

5. Gifts to Non-Citizens. This is a niche, but important if it applies. Gifts to non-citizen spouses have different rules. For the aual exclusion, the limit for gifts to a non-citizen spouse was $175,300 in 2024. It’s indexed for inflation too. Bigger than the standard aual exclusion, but still way less than what you can give to a citizen spouse without touching your lifetime exemption. It’s a whole separate beast.

The Tax-Free Gift Limit 2026: A Peek at the Numbers (Projections)

Okay, so the IRS hasn’t dropped the official 2026 numbers yet. They usually do this in the fall of the preceding year. But based on inflation trends and historical data, we can make some educated guesses. And trust me, the guesses are important.

Here’s a look at where things have been and where they might be headed. Take this with a grain of salt, but it’s better than flying blind. The Tax Free Gift Limit 2026 is a moving target.

| Year | Aual Exclusion Per Person | Estimated Lifetime Exemption (Per Person) |

|---|---|---|

| 2024 | $18,000 | $13.61 Million |

| 2025 | $18,500 (Est.) | $13.7 Million (Est.) |

| 2026 (Pre-Reversion Guess) | $19,000 (Est.) | ~$6.0 – $7.0 Million (Est. if TCJA expires) |

| 2026 (Post-Reversion Adjusted) | $19,500 (Est.) | ~$6.2 – $7.2 Million (Est. if TCJA expires & adjusted) |

Disclaimer: These are ESTIMATES. The actual numbers will be released by the IRS. The biggest variable is whether Congress acts to extend the TCJA provisions. If they don’t, expect that lifetime exemption to plummet.

The Crucial Takeaway: Act Smart, Not Hasty.

The Tax Free Gift Limit 2026 is shaping up to be a beast. Especially for those who have significant assets. The potential drop in the lifetime exemption is the elephant in the room. Ignoring it is like ignoring a leaky roof. It’s goa get worse.

My advice? Don’t panic. But don’t sleep on it either. Talk to a qualified estate plaing attorney or a CPA who actually understands this stuff. They can help you navigate the complexities. They can help you structure your gifts and your estate plan to minimize tax burdens. It costs money, sure. But it’ll cost you way more to screw it up.

I saw a friend get blindsided once. Huge inheritance. He thought he had it all figured out. Didn’t account for state estate taxes. Didn’t account for capital gains on assets he had to sell to pay the bills. Ended up losing a third of what his parents left him. A third! Because he didn’t ask the right questions. Be better than that. Plan now. The Tax Free Gift Limit 2026 demands it.

Frequently Asked Questions

What is the aual gift tax exclusion for 2026?

While the official IRS figures for 2026 won’t be released until late 2025, it’s projected to be around $19,000 to $20,000 per recipient, adjusted for inflation. This is the amount you can give to anyone, each year, without using any of your lifetime gift and estate tax exemption.

How much can I gift in 2026 without paying taxes?

You can gift up to the aual exclusion amount ($19,000-$20,000 estimated for 2026) to as many people as you want without tax implications or using your lifetime exemption. If you exceed this amount, you’ll start using your lifetime exemption, which is projected to significantly decrease in 2026 if current tax laws expire.

Will the lifetime gift tax exemption drop in 2026?

Yes, it is highly likely. The generous lifetime exemption set by the 2017 Tax Cuts and Jobs Act is scheduled to sunset at the end of 2025. If Congress doesn’t act, the exemption is projected to revert to a much lower amount, potentially around $6 million, adjusted for inflation from 2011.

What happens if I exceed the gift tax limit in 2026?

If your gifts exceed the aual exclusion amount, the excess will be applied against your lifetime gift and estate tax exemption. If you exhaust your lifetime exemption, any further taxable gifts will be subject to gift tax, which is currently a maximum rate of 40%.

Do I need to file a gift tax return (Form 709) in 2026?

Yes, you must file Form 709 if you give gifts exceeding the aual exclusion amount ($19,000-$20,000 estimated for 2026) to any individual, or if you elect to split gifts with your spouse. You also need to file if you made gifts to a non-citizen spouse above the aual exclusion for them, or if you made gifts using a generation-skipping transfer tax exemption.